We have noticed a significant trend is emerging among property investors—many are offloading secondary or investment properties in favour of secured fixed-term or debenture investments, which provide greater flexibility in the short term.

This shift is being driven by a combination of rising costs, global economic uncertainty, and the appeal of higher fixed-income returns.

With property markets facing increased pressure from interest rate fluctuations and tighter lending conditions, investors are reconsidering their strategies and opting for more stable, predictable returns.

Fixed-term and debenture investments not only offer security but also allow investors to maintain liquidity and adapt to changing economic conditions more effectively.

Given the current market climate, we anticipate that this sentiment will persist for some time. Until economic stability improves or property market dynamics shift, many investors may continue favouring fixed-income alternatives over real estate holdings.

📉 Property Market Pressures

Below are some key points regarding the current state of the property market in New Zealand:

- Falling Yields: Auckland rental yields hover around 3-4% (before tax, maintenance, and compliance).

- Tighter Regulations: Stricter tenancy laws, interest rates, and new compliance costs are reducing returns.

- Liquidity Issues: Selling property takes time, while fixed-income investments offer more flexibility.

- Modest Recovery Outlook: After a flat 2024, New Zealand’s property market is expected to see moderate growth in 2025, with forecasts predicting increases between 5% and 8%.

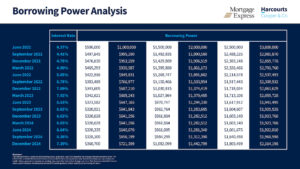

- Have you noticed that buyers aren’t offering as much as they used to? It’s not just a change in sentiment – it’s a direct result of borrowing power and rising interest rates.

- Borrowing Power Has Dropped – In June 2021, a buyer earning $500K could borrow $1M. By December 2023, that dropped to $641K.

Source: Harcourts

Source: Harcourts

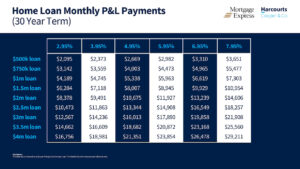

Higher Interest Rates = Higher Repayments – A $1M loan that once cost $4,189/month at 2.95% now costs $7,303 at 7.95%. Buyers’ budgets are stretched.

What This Means for Sellers:

Buyers are working with reduced budgets, making competitive offers less frequent.

Pricing your home correctly is more important than ever to attract serious buyers.

Properties that present great value will still sell, but expectations around pricing should be realistic.

📈 Global Economic Uncertainty

Since the start of the year, concerns over geopolitical tensions and the global economy have intensified. U.S. President Donald Trump’s sweeping regulatory changes have sparked global debate and left investors uncertain about the future.

Inflation is now a major concern, with economists predicting a surge following last week’s global tariffs, which could disrupt supply chains and drive up costs. Market volatility has escalated, adding to investor unease.

Recession fears are mounting after stock markets saw trillions wiped out in days.

Investors are reassessing strategies as bond yields fall, signalling a flight to safety.

Financial analysts warn that the coming months will be critical in determining whether these shocks are temporary or signs of a deeper downturn. Central banks may step in, but their ability to stabilise markets remains uncertain.

Some key points below:

Trade Tensions & Inflation Risks: Aggressive tariffs on imports have led to market volatility, supply chain disruptions, and increased inflationary pressures.

Stock Market Volatility: Recently, global stock markets have experienced significant declines, with over $3.7 trillion wiped off in the past week due to stagflation concerns.

Bond Market Signals: The yield on the two-year Treasury note has fallen to 3.89%, its lowest level since before President Trump’s second election, indicating a shift towards safer assets amid recession concerns.

Gold Prices Steady: Gold remains stable at $2,915.65 per ounce as investors await key U.S. inflation data.

🔻 Institutions Are Taking a Risk-Off Approach

Large investors and fund managers are increasingly shifting away from equities and high-risk assets in favour of more stable investments. This shift is being driven by several key factors:

Elevated Stock Valuations: Nearly half of institutional investors believe current stock prices are overvalued, raising concerns about potential market corrections.

Geopolitical Uncertainty: Rising global tensions, trade disputes, and ongoing conflicts are adding to financial instability, prompting investors to seek safer alternatives.

Market Volatility: A recent $759 billion selloff in major tech stocks has signalled growing risk aversion, with investors becoming more cautious about their exposure to high-growth sectors.

As uncertainty continues to dominate the global economic landscape, institutional investors—often regarded as “smart money” are prioritising stability. This has led to increased demand for high-yield secured investments, which offer predictable returns and reduced exposure to market fluctuations.

With volatility persisting, this risk-off sentiment may remain a defining trend in institutional portfolio strategies for the foreseeable future.

Interested in finding out how to get higher gains with less risk?

Fill in the form below

Join the Discussion

Type out your comment here:

You must be logged in to post a comment.