Most Kiwis have a “she’ll be right” attitude to their finances and figure that when the time comes they can sell down the family home, move into something smaller, and live off the proceeds.

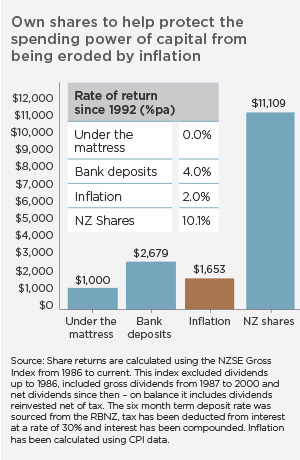

Another mistake Kiwi’s make is to withdraw from their KiwiSaver schemes and put those funds in term deposits and interest bearing bank accounts. A decade ago that meant 8.5 per cent returns, while now it means 3-4 per cent. This equates to a 60 per cent pay cut. This pay cut means you’ll have to use more of your capital sooner so it is going to get eaten up faster, says Stephen Jonas, Head of Client Services at Craigs Investment Partners.

Worrying trends for retirement security

There are three worrying trends amongst retired Kiwi investors:

- the emphasis on depositing all their capital with the banks;

- a last minute stretch of income by taking on greater risk; and

- a fear of seeking advice.

Last minute stretch for large returns: When retirees see their capital dwindling there can be a real risk that they “stretch for income”. That means investing their remaining capital in riskier investments in the hope of earning more. This is a dangerous strategy that could be avoided by investing wisely earlier on, or taking a longer term investing outlook.

Fear of seeking advice: Too often Kiwis fail to develop a plan for their money. Most Kiwis fail to plan to build sufficient capital for retirement, then fail to plan for the inevitable ups and downs of economies and markets once retired, says Jonas. Many Kiwis seem to fear seeking financial advice: they believe they don’t have sufficient money to invest, fear they will be sold something they don’t need, while some simply fear having to face the reality of their situation.

Seeking Advice

Engaging an Investment Adviser is a bit like going to the doctor or dentist. The sooner you seek the advice, the better the outcome. “We suggest you engage a qualified Investment Adviser to look at all your assets and help you understand how you can best structure your investments.” says Jonas. “It will cost you nothing to discuss your initial needs with an investment adviser, to consider your investment objectives and risk profile, and then have the Adviser recommend a suitable investment strategy, balancing risks with return.” It’s an Advisers job to overcome our behavioural biases and impartially assess your personal financial position. “While clients are ultimately in control, an Adviser’s role is to understand a client’s needs, draw on resources and recommend an investment strategy.” says Jonas.